Maria Shepherd, President and Founder, Medi-Vantage04.22.24

While sales and marketing of capital equipment in the medtech industry is still not a cakewalk, a survey (n=40 hospital administrators with purchasing decision power) from BTIG presents a light at the end of the tunnel.1

Eighty percent of these executives reported increases in surgical procedure volume in 2024 (low/mid-single percent)—a welcome forecast. Staffing shortages are still with us, which negatively affects procedure volumes, but at a lower percentage (33%) than 2023. In addition, the preponderance of these hospital administrators stated revenue growth in 2023 was ~5% and the majority expect the same revenue growth in 2024.1

These hospital administrators anticipate a relatively small increase in their capital equipment budget in this year and 2025, though a small segment of large hospital executives reported a larger budget increase.1

ResMed’s CEO Mick Farrell disclosed to the audience that ResMed is a company that manufactures cloud-connected devices that treat sleep apnea and COPD. The company’s products are called AirSense and AirCurve, and one of its key sales drivers is the myAir app.

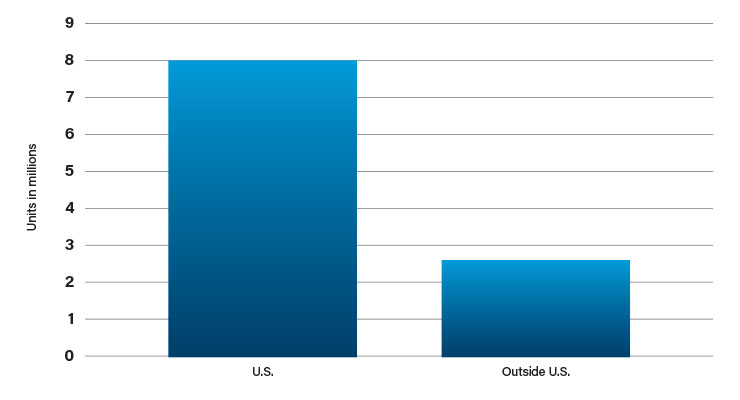

According to a U.S. Securities and Exchange Commission report, greater than 8 million CPAP devices are sold every year in the U.S., and another 2.5 million are sold worldwide (Table 1). In addition, there are an estimated 80 million more people with undiagnosed sleep apnea.4 Obstructive sleep apnea greatly reduces the quality of sleep each person enjoys and can result in serious complications like heart failure, stroke, and hypertension.

Farrell informed the audience his CPAP team switched from believing patient data was something to be monetized to a mindset of providing important data to patients. This benefit is a competitive advantage protecting ResMed’s share of market in the CPAP space. The myAir app is exclusive to AirSense and AirCurve CPAP users.

The myAir app is a form of gamification that Farrell reported ResMed patients are excited to use with their CPAP to see what their sleep scores are. In addition, ResMed obtains the patient data to use for analytical purposes that could yield new devices that improve patient outcomes and reduce costs.

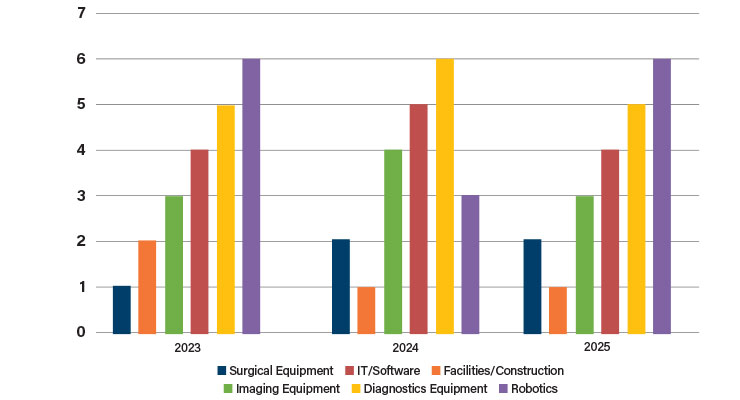

In addition, they noted their top six purchasing priorities—surgical equipment, facilities and construction, imaging equipment, IT and software, diagnostics and testing equipment, and robotics (Table 2). While shifting position during the years of 2023 to 2025, these items remain consistent top categories over those periods.1

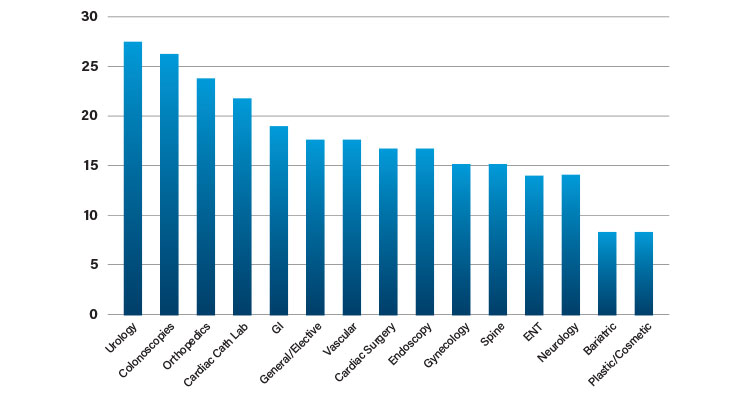

Of the 40 survey respondents, ~68% said urology procedures were running at full capacity and 65% said the same for colonoscopies. This was followed by orthopedics, the cardiac cath lab, GI, general and elective surgery, vascular, cardiac surgery, endoscopy, gynecology, spine, ENT, neurology, bariatric, and plastic/cosmetic.

References

Maria Shepherd has more than 20 years of experience in marketing in small startups and top-tier companies. She founded Medi-Vantage, which provides marketing and business strategy for the medtech industry. She can be reached at mshepherd@medi-vantage.com. Visit her website at www.medi-vantage.com.

Eighty percent of these executives reported increases in surgical procedure volume in 2024 (low/mid-single percent)—a welcome forecast. Staffing shortages are still with us, which negatively affects procedure volumes, but at a lower percentage (33%) than 2023. In addition, the preponderance of these hospital administrators stated revenue growth in 2023 was ~5% and the majority expect the same revenue growth in 2024.1

These hospital administrators anticipate a relatively small increase in their capital equipment budget in this year and 2025, though a small segment of large hospital executives reported a larger budget increase.1

Why Is This Important?

As I mentioned in an MPO Datawatch column (July 2023), the years following the pandemic proved challenging for hospital and personal-use capital equipment sales.2 Fortunately, there have been many new strategies to compete successfully in this space.3 At the 2022 AdvaMed annual meeting in Boston, the CEOs Unplugged panels were a fountain of information for developing new strategies for the medtech capital equipment space. As always, superior strategic, out-of-the-box thinking can turn market obstacles—including capital equipment sales—around.ResMed’s CEO Mick Farrell disclosed to the audience that ResMed is a company that manufactures cloud-connected devices that treat sleep apnea and COPD. The company’s products are called AirSense and AirCurve, and one of its key sales drivers is the myAir app.

According to a U.S. Securities and Exchange Commission report, greater than 8 million CPAP devices are sold every year in the U.S., and another 2.5 million are sold worldwide (Table 1). In addition, there are an estimated 80 million more people with undiagnosed sleep apnea.4 Obstructive sleep apnea greatly reduces the quality of sleep each person enjoys and can result in serious complications like heart failure, stroke, and hypertension.

Farrell informed the audience his CPAP team switched from believing patient data was something to be monetized to a mindset of providing important data to patients. This benefit is a competitive advantage protecting ResMed’s share of market in the CPAP space. The myAir app is exclusive to AirSense and AirCurve CPAP users.

The myAir app is a form of gamification that Farrell reported ResMed patients are excited to use with their CPAP to see what their sleep scores are. In addition, ResMed obtains the patient data to use for analytical purposes that could yield new devices that improve patient outcomes and reduce costs.

Response from Hospitals

In the BTIG survey, 85% of hospital administrators stated they regularly ask vendors or capital equipment sales representatives for reduced prices, flexible payment plans, and options to lease or rent. Many stated this is a process they always follow and included negotiating service contracts for maintenance, longer warranties, delayed billing, the routine expectation of discounts of 5%-10%, no interest terms, resolving older accounts payable at a discount, and strong value analysis committees.1In addition, they noted their top six purchasing priorities—surgical equipment, facilities and construction, imaging equipment, IT and software, diagnostics and testing equipment, and robotics (Table 2). While shifting position during the years of 2023 to 2025, these items remain consistent top categories over those periods.1

Staffing Shortage in Decline

A significant percentage of hospital decision-makers (68%) stated their hospital’s procedure volumes were no longer being impacted by staffing shortages.1 This resonates with what we learned throughout 2023 at meetings and through our 2023/2024 research with hospital administrators. BTIG research supported this finding as its March 2023 survey results revealed 75% of hospital administrators said procedure volumes were being impacted by staffing shortages. In that same survey, two out of three respondents (66%) said their organizations weren’t running at full capacity at some point over the past year due to staffing shortages. In addition, 70% said they were keeping patients in emergency departments due to a lack of staffing or bed capacity.Of the 40 survey respondents, ~68% said urology procedures were running at full capacity and 65% said the same for colonoscopies. This was followed by orthopedics, the cardiac cath lab, GI, general and elective surgery, vascular, cardiac surgery, endoscopy, gynecology, spine, ENT, neurology, bariatric, and plastic/cosmetic.

The Medi-Vantage Perspective

It’s wonderful news that greater than 50% of hospital administrator respondents expect to balance capex spending throughout 2024. Expect a great rush by sales reps to get into the hospital to promote their technology. Work toward differentiating your capital equipment with apps or other meaningful technologies that provide important benefits to the end users. It’s not too late to invest in Voice of the Customer or other research methodologies that provide insights on how you can accomplish this.References

Maria Shepherd has more than 20 years of experience in marketing in small startups and top-tier companies. She founded Medi-Vantage, which provides marketing and business strategy for the medtech industry. She can be reached at mshepherd@medi-vantage.com. Visit her website at www.medi-vantage.com.